Key Takeaways: Your Coverage Decision Guide

- Assessment Score: Check your “Summary of Benefits” specifically for Residential and Outpatient tiers to determine your baseline coverage.

- Success Factors: Prioritize In-Network providers to secure 120–200% reimbursement rates versus limited out-of-network coverage.

- Immediate Action: Call the number on the back of your card today and ask the “5 Critical Questions” listed in Section 2.

- Documentation: Always request written confirmation of benefits (email or letter) to prevent future denial disputes.

Understanding Your Health Insurance Coverage Landscape

Navigating health insurance for addiction treatment requires understanding the complex framework of healthcare benefits that govern what services are available and how they’re accessed. The landscape has evolved significantly since the Affordable Care Act and Mental Health Parity and Addiction Equity Act established requirements for insurers to cover substance use disorder treatment at levels comparable to other medical conditions.

Most insurance plans categorize addiction treatment services into distinct tiers, each with different coverage parameters. Inpatient or residential treatment typically falls under hospital or facility-based care benefits, while outpatient programs may be classified alongside other ambulatory services. Medication-assisted treatment often appears under both pharmacy benefits and medical care, creating multiple pathways for coverage that can be confusing to decipher.

| Plan Type | Flexibility | Key Constraint |

|---|---|---|

| PPO (Preferred Provider) | High | Higher premiums; staying in-network yields better benefits. |

| HMO (Health Maintenance) | Low | Strict network limits; referrals often required for specialized care. |

| HDHP (High Deductible) | Moderate | High upfront costs before coverage activates (often paired with HSA). |

Coverage limitations vary widely between plans and insurers. Some policies impose strict limits on the number of treatment days or sessions allowed annually, while others use medical necessity criteria to determine appropriate care duration. Prior authorization requirements add another layer, requiring approval before treatment begins to ensure services meet plan guidelines.

Understanding these foundational elements provides the necessary context for evaluating personal coverage. The specific benefits available depend on the interplay between plan type, network participation, deductible status, and individual policy terms. This knowledge becomes essential when assessing whether current coverage aligns with treatment needs and what financial responsibilities to anticipate throughout the recovery journey.

How the ACA Changed Rehab Coverage

The Affordable Care Act (ACA) transformed the way insurance plans address rehab by requiring all Marketplace policies to include substance use treatment as a core benefit. Before the ACA, many people found that their insurance offered little to no help for addiction or wellness-related care. Now, every plan sold through the federal or state exchanges must cover services like inpatient rehab, outpatient therapy, and counseling under what are known as “essential health benefits”1.

This approach works best when individuals want predictable coverage and fewer surprise exclusions, especially for those shopping in the Marketplace or considering Medicaid expansion plans. Still, research shows that while the ACA set a national baseline for what must be covered, the exact scope, network options, and cost-sharing details can look quite different from one plan to another4. Up next, let’s break down what these essential benefits include and how federal parity laws further shape your options.

Essential Health Benefits Explained

Here’s a quick checklist to help understand what “essential health benefits” include when it comes to substance use treatment:

- Inpatient rehab

- Outpatient therapy

- Counseling

- Supportive wellness services

These are all required to be covered by every ACA Marketplace plan1. The law defines these benefits to make sure that core rehab and wellness services can’t be excluded, though plans still set their own networks and cost-sharing details. Industry leaders find that this structure ensures most people with private or Medicaid insurance now have access to care that was often out of reach before the ACA4.

If you’re sorting through plan options, keep in mind that while major categories are mandated, the specific treatments and where you can go for care may differ. This path makes sense for those who want clarity on what services are guaranteed before committing to a particular insurance plan. Next, let’s see how parity laws work to prevent unfair limits on these covered benefits.

Parity Laws & What They Protect

Parity laws—officially known as the Mental Health Parity and Addiction Equity Act (MHPAEA)—require that health insurance plans treat rehab and wellness benefits the same as medical or surgical care. This means your insurer can’t set stricter limits, higher copays, or shorter coverage periods for substance use treatment than they do for physical health services3.

In practice, parity rules protect you from yearly caps or tight visit limits that don’t apply elsewhere in your plan, and they also prevent plans from using more restrictive approval processes just for rehab care. As of 2024, new federal rules strengthen these protections by demanding insurers prove equal access to behavioral health and wellness services, making it harder for plans to quietly limit coverage3. This approach works best for people who want confidence that their insurance plan can’t unfairly restrict access to necessary rehab support.

Coverage Gaps Still Exist in 2025

Even in 2025, many people with health insurance encounter real barriers when trying to use their coverage for rehab and wellness services. One practical tool to assess your risk: ask your provider about their average claim denial rate and whether they require extra approvals for treatment.

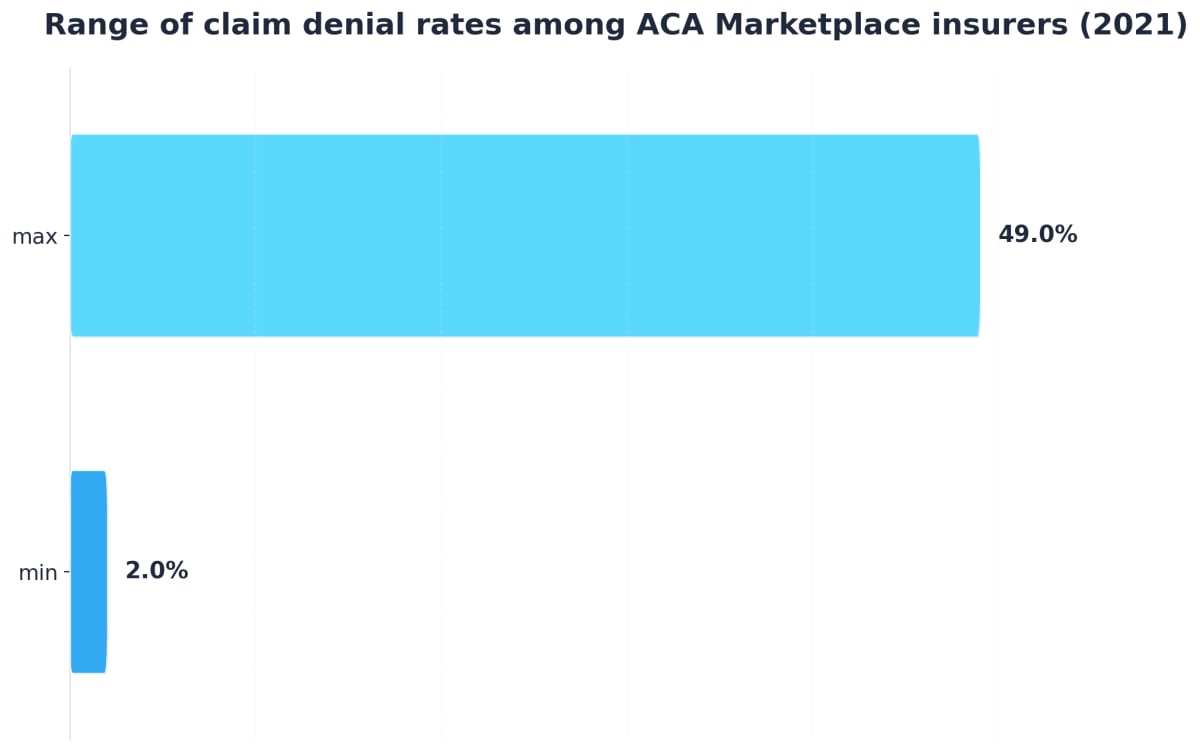

Research shows that nearly 17% of in-network claims on ACA Marketplace plans are denied, with denial rates swinging from just 2% up to 49% depending on the insurer6.

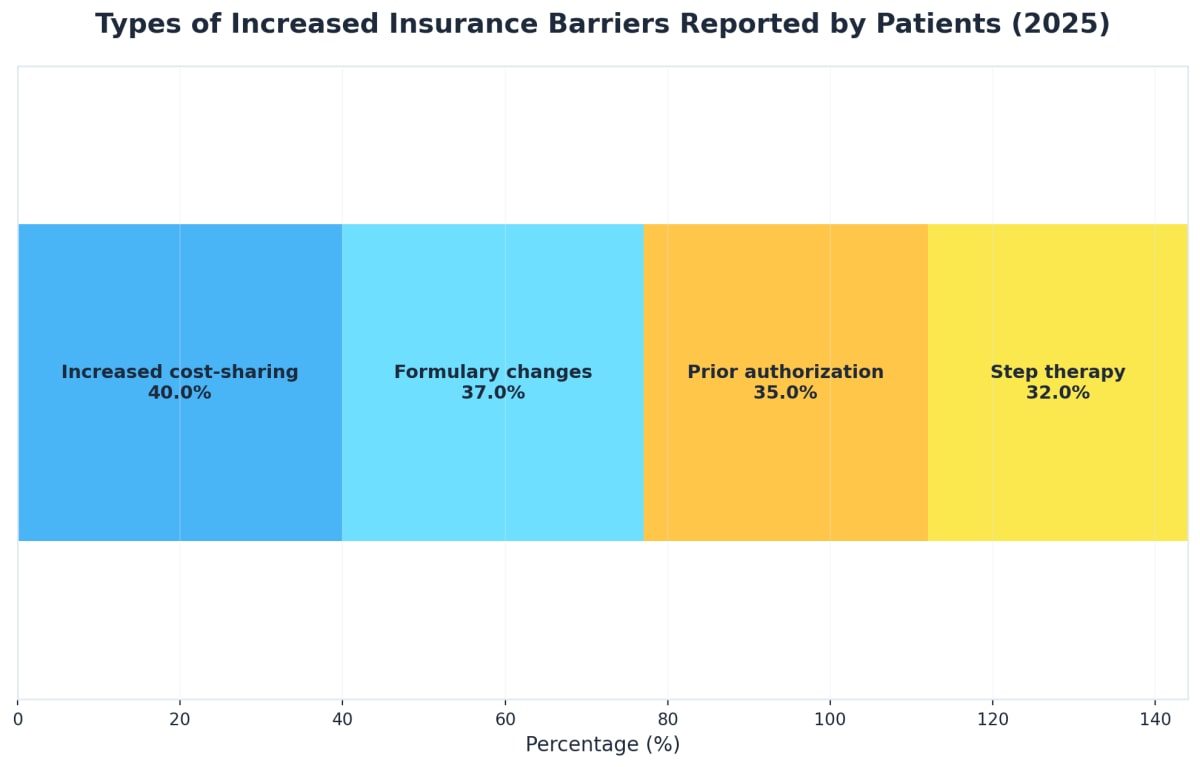

These denials often aren’t about medical necessity but stem from vague reasons or missing authorizations. On top of that, about 35% of adults with chronic conditions say they’re facing more barriers—like higher cost-sharing and stricter formulary rules—compared to last year5. This situation fits those who want to avoid added costs or delays and underscores why understanding your insurance network and approval processes matters. Next, we’ll unpack why claims get denied and how coverage rules differ across states.

Why 17% of Claims Are Denied

The reasons behind the 17% denial rate for in-network claims in ACA Marketplace plans are more complex than many expect. While readers might assume most denials stem from medical necessity, research reveals that just 2% are due to those criteria. Instead, 14% of denials relate to excluded services, 8% are about missing preauthorization or referrals, and a striking 77% fall into the vague category of ‘all other reasons’6.

This lack of clarity can leave individuals frustrated and unsure how to address the problem. Common scenarios include paperwork errors, billing code mismatches, or unclear documentation. This situation fits people who want to minimize surprise costs and delays—especially those navigating private insurance or Medicaid plans. As we move forward, understanding how coverage rules change from state to state becomes crucial for anyone relying on insurance for wellness or rehab support.

State-by-State Medicaid Variations

Medicaid coverage for rehab and wellness services can look very different depending on where you live. Here’s a quick assessment tool: check your state Medicaid website to see which services are included, whether there are session limits, and if certain treatments—like group therapy or residential stays—are covered.

Studies reveal that treatment rates for Medicaid enrollees with a substance use diagnosis range widely, from 53% in some states up to 89% in others7. These gaps come from state-level choices about what’s funded, the size of provider networks, and how strict approval rules are. This solution fits people who want to maximize their wellness options through public insurance and avoid unexpected out-of-pocket costs. Moving ahead, it’s wise to compare your plan’s specifics directly with state guidelines to clarify what’s actually available.

Self-Assessment: Does Your Health Insurance Plan Cover Treatment?

With this coverage framework in mind, the next step is evaluating your specific policy details. Most health insurance plans provide some level of coverage for addiction treatment, but the extent varies significantly based on your plan type, provider network, and individual policy terms.

Start by locating your insurance card and policy documents. Look for the customer service number on the back of your card—this direct line to your insurance provider offers the most accurate information about your benefits. When you call, ask specific questions about residential treatment coverage, including whether pre-authorization is required, what your deductible and out-of-pocket maximum are, and which facilities fall within your network.

Your Summary of Benefits and Coverage (SBC) document provides another valuable resource. This standardized form outlines your plan’s coverage for various healthcare services. Pay particular attention to sections covering inpatient care, outpatient services, and any exclusions or limitations that might apply to substance use disorder treatment programs.

Many insurance companies also offer online portals where you can verify benefits, check claim status, and review coverage details at your convenience. These digital tools often include provider directories that help you identify in-network facilities, potentially saving thousands of dollars compared to out-of-network options.

Consider these key questions during your self-assessment: Does your plan require a referral from your primary care physician? Are there visit limits or duration caps on residential treatment? What percentage of costs will you be responsible for after meeting your deductible? Understanding these details upfront prevents unexpected bills and helps you budget appropriately.

If your current plan offers limited coverage, explore whether supplemental insurance or employee assistance programs through your workplace might provide additional benefits. Some employers offer enhanced addiction treatment benefits that extend beyond standard health insurance, creating more comprehensive coverage options for treatment services.

Five Questions to Ask Your Insurer

When you’re ready to use your health insurance for rehab or wellness support, having a focused set of questions for your insurer can make all the difference. Start with this five-question checklist:

- Are detox and residential rehab covered as part of your benefits?

- What outpatient programs or medication-assisted treatments are included?

- Do you need prior authorization before starting care?

- Which providers are considered in-network for these services?

- What out-of-pocket costs—like deductibles or copays—should you expect?

Studies reveal that the details behind these answers can vary sharply, even for similar insurance plans, and that nearly 17% of in-network claims may still be denied for reasons like authorizations or network issues4, 6. If you want to avoid costly surprises and delays, this strategy suits anyone using private insurance or Medicaid for treatment. Next, you’ll see how to dig deeper into your policy documents to confirm exactly what’s covered.

Verify Detox & Residential Benefits

To confirm whether your plan supports detox and residential rehab, start by asking your insurer for a detailed list of covered wellness services and any approval steps required before admission. Not all health plans treat these benefits equally—research highlights that while ACA Marketplace and Medicaid plans must include inpatient care as an essential benefit, the specific coverage and session limits can differ sharply by state and insurer1, 4.

If you have private coverage, check for requirements like prior authorization or network restrictions, as these are common hurdles linked to higher denial rates6. This method works when you need reliable answers about which levels of care are supported and want to minimize the risk of surprise bills. To strengthen your understanding, ask for documentation about what is included under “detox” and “residential” support, since definitions and covered amenities may vary.

Check Outpatient & MAT Coverage

To check if your insurance plan covers outpatient programs and medication-assisted treatment (MAT), request a clear breakdown of which services qualify as outpatient care and which medications are approved for recovery support. While most Marketplace and Medicaid plans must include outpatient care among their essential health benefits, the range of covered services—such as counseling, group sessions, and MAT options like buprenorphine or naltrexone—can differ significantly by insurer and state1, 4.

Industry research shows that neither all private nor all public insurance plans cover every MAT medication, and session limits or step therapy rules may apply4. This solution fits those who want to access flexible, step-down care while staying within network and minimizing unexpected bills. For the best results, ask your insurer to specify which outpatient and MAT providers are in-network and whether you’ll need prior authorization for these wellness services.

Decoding Your Policy Documents

Decoding your policy documents is a crucial step in confirming what your insurance actually covers for rehab and wellness services. Start with this quick-reference tool: identify and highlight sections in your Summary of Benefits and Coverage (SBC) that mention inpatient, outpatient, and supportive wellness benefits.

Look for terms like prior authorization, network provider, and exclusions—these signal where coverage or approval rules may apply. Research shows that nearly 17% of in-network claims are denied, often due to missing authorizations or unclear documentation rather than true benefit limits6. This strategy suits anyone who wants to avoid unnecessary denials and spot potential hurdles early. By carefully reviewing your SBC and plan booklet, you’ll be prepared to ask focused questions and clarify details before committing to any treatment program. Next, we’ll look more closely at how prior authorization and network rules can impact your access to covered services.

Prior Authorization Requirements

Prior authorization is an approval step that insurance plans require before they’ll pay for certain rehab or wellness services. Here’s a quick assessment tool: check your Summary of Benefits and Coverage for mentions of prior authorization next to inpatient, outpatient, or specific therapies.

Industry analysis finds that prior authorization is a key reason why 8% of in-network claims get denied on ACA Marketplace plans, with missing or delayed approvals often causing unexpected out-of-pocket costs6. If your plan lists prior authorization for a service, you’ll need to submit paperwork—sometimes including medical records or a provider’s referral—before starting care. This method works when you want to avoid claim denials and delays, especially if you’re using private insurance or Medicaid for rehab or wellness support. Next, it’s vital to look at how network restrictions can further impact your access to covered treatment.

Understanding Network Restrictions

Understanding network restrictions is key to making the most of your health benefits. Use this quick decision guide: check your Summary of Benefits and Coverage for the terms “in-network” and “out-of-network”—these mark where your insurance will cover the most, or where you might face higher bills.

Research shows that denial rates for in-network claims range widely, from just 2% up to 49%, depending on the insurer, often because care was received out-of-network or the provider wasn’t properly listed6. This solution fits those who want to avoid costly surprises and maximize their wellness options by choosing in-network providers whenever possible. If you’re unsure, call your insurer to verify that your preferred rehab or wellness provider is currently in-network and confirm any referral requirements. Next, you’ll see how to match your chosen treatment level with your insurance plan for the smoothest coverage experience.

Decision Framework: Choosing Your Path

After understanding your insurance coverage and the financial implications of different treatment options, the next step involves translating that knowledge into an informed treatment decision. The coverage differences you’ve discovered—whether your plan offers more comprehensive benefits for inpatient care, requires different cost-sharing for outpatient services, or imposes authorization requirements—should factor into your decision framework alongside medical and personal considerations. This integrated approach ensures that both clinical needs and financial realities align to support sustainable recovery.

Making the decision between inpatient and outpatient treatment represents a critical turning point in recovery. This choice impacts not just the immediate treatment experience, but also long-term outcomes and quality of life during the healing process.

The decision framework starts with medical necessity. If withdrawal symptoms pose health risks, if previous outpatient attempts haven’t succeeded, or if the home environment lacks stability, inpatient care becomes the clear choice. Medical professionals can assess these factors during initial consultations, providing objective guidance based on clinical criteria rather than preferences alone.

Financial considerations play a practical role in this decision. Insurance coverage varies significantly between inpatient and outpatient programs, and understanding these differences before committing to treatment prevents unexpected financial stress. Many facilities offer verification services that clarify coverage details, out-of-pocket costs, and payment options within 24 hours of inquiry.

Personal circumstances deserve equal weight in the decision process. Employment obligations, family responsibilities, and support system availability all influence which treatment model fits best. Someone with strong family support and a stable living situation may thrive in outpatient care, while another person facing housing instability might need the structure of residential treatment.

The severity and duration of substance use also guide this choice. Long-term dependencies or polysubstance use patterns often require the intensive intervention that inpatient programs provide. Conversely, those in earlier stages of dependency with strong motivation and external support may achieve successful outcomes through outpatient treatment.

Ultimately, this decision benefits from professional input. Treatment centers conduct comprehensive assessments that evaluate medical history, substance use patterns, psychological factors, and social circumstances. These assessments provide personalized recommendations that balance clinical needs with practical realities, creating a foundation for informed decision-making that supports lasting recovery.

Match Treatment Level to Your Needs

Choosing the right level of care is simpler with a step-by-step decision tool: review your insurance plan’s Summary of Benefits and Coverage to identify if residential rehab, outpatient care, or a hybrid approach is supported. Plans often describe these options in sections labeled “inpatient,” “outpatient,” or “partial hospitalization.”

Coverage varies—Medicaid typically reimburses wellness providers at 70-80% of Medicare rates, while commercial insurers may pay between 120-200% of Medicare, but only for approved service levels and in-network providers2. This method works when you want to ensure your benefits align with your lifestyle, work needs, and available support. If you’re balancing job responsibilities, outpatient or virtual programs could offer flexibility, while residential care may be best for those needing routine and structure. By matching your needs to the right setting, you position yourself for the best insurance experience and minimize unnecessary costs. Up next, let’s estimate the specific resources and expenses required for each type of care.

When Residential Care Is Covered

A practical way to determine if residential care is covered by your insurance is to use a quick eligibility checklist:

- Look for “inpatient” or “residential” sections in your plan’s Summary of Benefits and Coverage.

- Check if your insurer requires prior authorization for this level of care.

- Confirm the provider is in-network, since out-of-network stays are often excluded or reimbursed at much lower rates.

Medicaid programs typically pay residential wellness providers at 70-80% of Medicare rates, while commercial insurance may reimburse between 120-200% of Medicare benchmarks, but access depends on approval and plan limits2. This route works well for those who need a structured environment and want their insurance to help manage the cost of longer stays. If your policy has session or day limits, ask about extensions or exceptions, as these can make a difference in your recovery journey. Next, let’s look at how outpatient programs support adults balancing treatment with work or family responsibilities.

Outpatient Options for Working Adults

For working adults, outpatient rehab and wellness programs offer a flexible way to maintain employment and family life while receiving ongoing support. A practical assessment tool: review your plan’s Summary of Benefits and Coverage for sections labeled “outpatient,” “intensive outpatient,” or “partial hospitalization” to see what levels are covered and whether virtual options are included.

Industry research finds that Medicaid usually reimburses outpatient care at about 70-80% of Medicare rates, while commercial insurance pays 120-200% of Medicare benchmarks, but coverage is only guaranteed for in-network, approved services2. This strategy suits those who need to schedule treatment around job commitments or prefer step-down care that fits their routine. Ask your insurer if telehealth or evening sessions are included, as remote programs now make up at least 38% of all behavioral health visits and are widely supported by insurance plans2. Up next, let’s estimate the resources and expenses for each treatment type to help you plan ahead.

Resource Planning & Cost Estimates

Resource planning for rehab and wellness services starts with a simple checklist:

- Review your Summary of Benefits and Coverage for out-of-pocket details.

- Confirm reimbursement rates for in-network providers.

- Identify any required authorizations or limits on sessions.

Medicaid typically reimburses wellness and rehab providers at 70–80% of Medicare rates, while commercial plans may pay between 120–200% of Medicare, but only for approved, in-network services2. Industry analysis notes that increased cost-sharing and prior authorization are among the most common insurance barriers reported by 35% of adults with chronic conditions in 20255.

This strategy suits those who need to forecast direct expenses and align their budget with available coverage. To make a clear plan, also consider whether nonprofit or for-profit providers match your needs, as pricing structures and insurance acceptance can differ. Up next, you’ll see how to estimate your actual out-of-pocket costs and compare nonprofit versus for-profit options.

What You’ll Pay Out-of-Pocket

Estimating your out-of-pocket costs for rehab and wellness services with health insurance starts with three key factors: your plan’s cost-sharing rules, provider network status, and any prior authorization requirements. Industry research reveals that increased cost-sharing—such as higher deductibles or copays—is the most common insurance barrier reported by 40% of adults with chronic conditions in 20255.

Medicaid typically covers 70–80% of Medicare rates, while commercial plans may pay 120–200% of Medicare, but you’ll still owe any copays, coinsurance, or amounts above annual coverage caps2. Opt for in-network providers to keep your share as low as possible, since out-of-network care is often excluded or reimbursed at much lower rates. This solution fits anyone wanting to forecast expenses and avoid surprise bills; always confirm your plan’s details before starting care. Next, you’ll compare how nonprofit and for-profit providers structure their pricing and work with insurance.

Nonprofit vs. For-Profit Pricing

When comparing nonprofit and for-profit rehab providers, there are a few practical differences that can impact your total costs and how your health insurance is used. Start with this quick assessment tool:

- Ask if the provider is in-network with your insurance.

- Request details about any sliding-scale or reduced fees for those with high deductibles.

- Clarify whether they accept Medicaid or commercial insurance for wellness services.

Research shows that for-profit centers may be more likely to charge at the higher end of commercial reimbursement rates—often 120–200% of Medicare—while nonprofit organizations usually accept Medicaid, which reimburses at 70–80% of Medicare, and may offer lower or flexible fees for eligible clients2. This strategy suits those who want to optimize their insurance coverage and control out-of-pocket expenses, as nonprofit programs often provide more transparency around pricing and may have additional financial support options. To choose the best fit, weigh both the provider’s insurance acceptance and their approach to billing, as this can make a significant difference in your wellness planning. Next, you’ll move into implementation: what to do in your first 30 days to secure coverage and avoid common pitfalls.

Implementation: Your Next 30 Days

The first thirty days after choosing a recovery program set the foundation for long-term success. Breaking this critical period into manageable phases helps reduce overwhelm and creates momentum from day one.

During week one, focus on logistics and preparation. Contact your chosen facility to confirm admission dates, complete required paperwork, and clarify what to bring. This is when thorough insurance verification becomes essential. Call the member services number on the back of your insurance card and ask specific questions: What is the prior authorization timeline for residential treatment? Is your chosen facility in-network, and if so, what’s your financial responsibility—a flat copay or coinsurance percentage?

Request written confirmation of your coverage details and the authorization reference number. For example, you might learn you have a $250 copay for the first day plus 20% coinsurance after your deductible, with a maximum out-of-pocket of $3,000—information that helps you plan financially. Also ask whether your plan requires step-down verification for different levels of care, so you’re not surprised if transitioning from residential to outpatient later. Arrange time off from work or school, and have honest conversations with family members about your treatment timeline. If you have dependents, finalize childcare arrangements. Set up payment plans with the facility if needed, and ensure bills will be paid during your absence.

Week two shifts to personal preparation. Begin adjusting your sleep schedule to match the program’s routine, as many facilities start early. If you’re currently using substances, consult with medical professionals about safe discontinuation protocols. Follow up on any outstanding insurance authorizations—contact the facility’s admissions team to confirm they’ve received approval and clarify exactly what your first payment will be on admission day. Pack comfortable clothing, any approved medications with proper documentation, and personal items that provide comfort within facility guidelines. Write down your reasons for seeking treatment and your recovery goals—you’ll reference these when motivation wavers.

The third week typically marks program entry. Expect an adjustment period as you acclimate to new routines, meet staff and peers, and begin participating in therapeutic activities. Stay open to the process even when it feels uncomfortable. Building connections with others in recovery often provides unexpected support and perspective.

By week four, you’re establishing rhythm within the program structure. Focus on active participation in all sessions, honest communication with counselors, and applying new coping strategies. This is when many people experience breakthrough moments in understanding their relationship with substances and identifying patterns that need to change. Trust the process, lean on the support around you, and remember that recovery unfolds one day at a time.

Week 1: Verify Benefits & Get Pre-Auth

Kick off your 30-day plan with a focused benefits check and pre-authorization process—these steps can make all the difference in accessing rehab or wellness services through your health insurance. Start with this actionable checklist:

- Call your insurer using the number on your insurance card.

- Ask for a detailed explanation of your coverage for rehab, outpatient, and supportive wellness services.

- Confirm if pre-authorization is needed and request the paperwork if so.

- Make sure your chosen provider is in-network to avoid unnecessary costs.

Studies reveal that 35% of adults with chronic conditions face increased insurance barriers like prior authorization and cost-sharing in 2025, so taking these steps early can help you avoid delays and denials5. This strategy suits anyone who wants to secure coverage and reduce out-of-pocket expenses before starting treatment. Next, you’ll see how to contact your insurer directly and request written confirmation of your benefits.

Contact Your Insurer Directly

Speaking directly with your insurer is one of the most reliable ways to clarify your coverage for rehab and wellness services. Use this step-by-step tool: call the customer service number on your insurance card, have your policy details on hand, and prepare your list of questions about covered services, in-network providers, and any pre-authorization steps.

Industry research shows that 35% of adults with chronic conditions in 2025 report increased insurance barriers—often related to unclear benefit details or new approval requirements5. This approach works best when you want clear, immediate answers and a record of your conversation. Be sure to ask the representative for their name, note the date and time, and request a call reference number for your records. After this call, you’ll be ready to formally request written benefit confirmation to avoid future disputes.

Request Written Benefit Confirmation

After speaking with your insurer by phone, requesting written benefit confirmation is a smart next step to protect yourself from misunderstandings about your rehab and wellness coverage. Here’s a practical tool: ask your insurer to provide a formal letter or secure email detailing your approved services, any required pre-authorizations, and your expected out-of-pocket costs.

Industry analysis finds that 35% of adults with chronic conditions in 2025 reported increased health insurance barriers—including prior authorization and unclear benefit details—which can lead to costly delays if not addressed up front5. This method works when you want documented proof of your coverage, especially if you’re preparing for treatment start dates or need to resolve billing disputes later. For best results, save all correspondence and double-check that written confirmation matches what was discussed by phone. As you move forward, you’ll be equipped to navigate denials or appeals if your insurer later disputes your eligibility or payment for services.

Weeks 2–4 are your window to tackle health insurance denials and start the appeals process with confidence. Use this practical tool: keep a claim tracker with dates, correspondence, and copies of all denial letters so you’re prepared for every step. Research shows that between 39% and 59% of internal appeals for denied claims are ultimately reversed in favor of the patient, making the effort well worth it8.

If your appeal is unsuccessful, you may be able to file an external review or contact your state insurance regulator for added support. This process suits anyone facing unexpected claim denials, especially those using private insurance or Medicaid for wellness or rehab services. By staying organized and persistent, you can increase your odds of overturning a denial and securing the benefits your plan promises. Next, you’ll get step-by-step guidance on how to file an appeal and when it’s time to involve your state’s regulatory agency.

File Internal Appeals Successfully

Filing an internal appeal for a denied claim starts with a clear, step-by-step tool:

- Review your denial letter for the specific reason and any instructions.

- Gather supporting documents such as provider notes and prior authorization records.

- Write a concise appeal letter explaining why your rehab or wellness service should be covered.

- Submit your appeal within your plan’s stated deadline, keeping copies of everything you send.

Studies reveal that between 39% and 59% of internal appeals are reversed in favor of the patient, so this effort can truly pay off8, 9. This method works well if you want to resolve issues directly with your health insurance company and avoid unnecessary escalation. Be sure to track all communications and follow up on your appeal’s status every week until you receive a written decision. Up next, you’ll find out when contacting your state insurance regulator becomes the right move.

When to Contact Your State Regulator

If your internal appeal for a denied claim is unsuccessful or you believe your health insurance isn’t following state or federal coverage rules, it may be time to involve your state insurance regulator. Use this quick assessment:

- Review your denial and appeal correspondence for evidence of unfair benefit limits or procedural delays.

- Check if your state offers an external review process.

- Gather all supporting documents before submitting a complaint.

Studies reveal that state regulators can step in when insurers persistently deny legitimate wellness claims or fail to comply with parity and transparency laws9. This route makes sense for anyone who has exhausted their plan’s appeals process or suspects noncompliance with required coverage for rehab and supportive wellness services. State insurance departments can often require insurers to conduct an independent review or even reverse a denial, helping you secure the benefits your plan is meant to provide. As you reach this stage, you’ll be well-prepared to advocate for fair treatment and move forward with your wellness journey.

Frequently Asked Questions

Navigating outpatient treatment options can raise many questions for individuals and families seeking support. Understanding the basics—especially regarding insurance coverage—helps make informed decisions about care.

What’s the difference between outpatient and inpatient treatment?

Outpatient programs allow participants to live at home and maintain daily responsibilities while attending scheduled treatment sessions. Inpatient or residential programs require staying at a facility full-time, typically for more intensive needs or when a structured environment is essential for safety and recovery.

How many hours per week does outpatient treatment require?

Time commitments vary by program level. Partial hospitalization programs typically involve 20-30 hours weekly, intensive outpatient programs require 9-15 hours, and standard outpatient care may involve just a few hours per week. The appropriate level depends on individual needs and treatment goals.

Can someone work or go to school during outpatient treatment?

Yes, maintaining employment and education is often possible and encouraged. Many programs offer flexible scheduling, including evening and weekend sessions, specifically designed to accommodate work and school commitments. This integration of treatment with daily life helps build practical recovery skills in real-world settings.

How long does outpatient treatment typically last?

Duration varies based on individual progress and needs. Some participants complete programs in a few weeks, while others benefit from several months of care. Many people transition through different levels of care, starting with more intensive support and gradually reducing hours as they build stability and confidence.

Will insurance cover outpatient treatment?

Most insurance plans provide coverage for outpatient wellness and substance use services under the Mental Health Parity and Addiction Equity Act, though specific benefits vary by policy. The verification process typically involves contacting your insurer to confirm coverage percentages (often 60-80% after deductible), copayment amounts, session limits, and network provider requirements.

Important questions to ask include: What is my deductible and out-of-pocket maximum? How many sessions are covered per year? Are there restrictions on program types? Does my plan require prior authorization? Treatment centers typically assist with insurance verification and can clarify coverage details before starting care.

What is prior authorization and how long does it take?

Prior authorization is a requirement by some insurance plans to approve treatment before it begins, ensuring the services meet medical necessity criteria. The process involves the treatment provider submitting clinical information to the insurance company for review. Standard prior authorizations typically take 3-5 business days, though urgent requests may be expedited within 24-72 hours. Some plans don’t require prior authorization for outpatient services, while others may need it only for higher levels of care like partial hospitalization programs. Checking this requirement during insurance verification prevents unexpected delays in starting treatment.

What does medical necessity mean for my coverage?

Medical necessity refers to the standard insurance companies use to determine whether treatment is appropriate and covered under your plan. For outpatient wellness or substance use treatment, medical necessity typically means services are clinically appropriate for your diagnosis, consistent with evidence-based standards of care, and provided at the right level of intensity for your condition. Providers document symptoms, functional impairment, and treatment goals to demonstrate medical necessity. Understanding this concept is important because services deemed not medically necessary may not be covered, even if your plan includes wellness benefits.

Will my insurance cover treatment if I have a pre-existing substance use condition?

Yes, under current federal law, your health insurance must cover treatment even if you have a pre-existing substance use condition. Thanks to the Affordable Care Act (ACA), all Marketplace health plans—and most employer-based and Medicaid options—cannot deny you coverage, charge you more, or put annual or lifetime dollar limits on treatment just because you have a history of substance use1. This protection applies to both new and existing members, making it easier for people to access rehab or supportive wellness services without fear of being turned away. Industry sources confirm that Marketplace plans specifically list substance use treatment as an essential health benefit, and parity laws require insurers to treat these services like any other medical care3. If you have questions about your plan’s rules, check your Summary of Benefits and Coverage or call your insurer for details.

Are there affordable options if I don’t have insurance or my plan won’t cover treatment?

Yes, there are practical and affordable options if you don’t have health insurance or your plan won’t cover rehab or wellness services. Many nonprofit treatment centers offer sliding-scale fees, which adjust costs based on your income. Some community health clinics and state-funded programs provide low-cost or free wellness support, especially for individuals who meet certain financial criteria. Studies reveal that nonprofit providers are often more likely to accept Medicaid or offer reduced fees compared to for-profit centers, making them a strong fit for people seeking cost-conscious care2. You might also find assistance through local or national support organizations, which can help connect you with grants or payment plans. This method works for anyone who needs flexible options beyond traditional health insurance and wants to avoid large upfront expenses while still accessing quality support.

Does insurance cover family therapy or support services during treatment?

Most health insurance plans do offer coverage for family therapy or support services as part of a rehab or wellness program, especially when these services are considered essential for the participant’s recovery. Under the Affordable Care Act, Marketplace and many employer-based policies must cover counseling and supportive wellness benefits, which often include family or couples sessions if recommended by the treatment provider1. Medicaid also frequently includes family support as a covered service, though the availability and limits can differ from state to state7. This makes insurance a good fit for those who want to involve loved ones in the process and strengthen support at home. To confirm what’s included, review your Summary of Benefits and Coverage or call your insurer to ask about family therapy, group support, or educational services connected to your rehab plan.

What documentation do I need to submit an appeal for a denied claim?

To submit an appeal for a denied claim, you’ll need to gather several key documents to build a strong case. Start with the denial letter from your insurer, which explains the reason for denial and outlines appeal instructions. Next, collect supporting materials such as your provider’s clinical notes, any prior authorization forms, and a detailed explanation from your doctor about why the recommended rehab or wellness service is necessary. It’s also wise to include your original claim paperwork and records of any phone calls or written communication with your insurance company. Research shows that appeals are more likely to succeed when all required documentation is submitted clearly and on time—between 39% and 59% of internal appeals for denied claims are ultimately reversed in favor of patients8, 9. By keeping copies of everything you send and following your plan’s stated deadlines, you increase your chances of overturning a denial and securing your health insurance benefits.

What should I do if my insurance denies coverage for recommended treatment?

If your insurer denies coverage for recommended rehab or wellness treatment, start by reviewing the denial letter to understand the specific reason. Often, denials result from missing paperwork, prior authorization issues, or vague explanations rather than a true lack of benefit6. The next step is to file an internal appeal with your health insurance company—gather supporting documents such as provider notes and prior approval records to strengthen your case. Research shows that between 39% and 59% of internal appeals are ultimately reversed in the patient’s favor, so pursuing an appeal can make a real difference8, 9. If your appeal isn’t successful, you may be able to request an external review or contact your state insurance regulator for additional help. This route is especially effective for those wanting to protect their wellness options and ensure fair access to covered services.

How much will I realistically pay out-of-pocket for rehab with insurance?

Out-of-pocket costs for rehab with insurance depend on your plan type, network status, and required approvals. Most people with Medicaid can expect coverage at 70–80% of Medicare’s benchmark rates, while commercial insurance often pays providers 120–200% of Medicare, but you’ll still be responsible for any copays, coinsurance, deductibles, or charges above annual caps2. Research shows that higher cost-sharing is the top insurance barrier for 40% of adults with chronic conditions in 2025, so it’s wise to confirm your plan’s details before starting care5. Choosing in-network providers and getting any needed pre-authorizations will help minimize unexpected expenses. If you’re weighing nonprofit versus for-profit centers, nonprofits may offer sliding-scale fees or accept Medicaid, which can further reduce your total responsibility. Always ask for a written estimate from your provider and check your Summary of Benefits and Coverage for specifics.

Does Medicaid cover the same substance use treatment services as private insurance?

Medicaid and private health insurance both cover substance use treatment, but the specific services and access can differ quite a bit. Medicaid is required to include rehab and wellness benefits, yet each state decides which services—like inpatient, outpatient, group therapy, or certain medications—are actually available. This leads to wide variation: in 2020, treatment rates for Medicaid enrollees with a substance use diagnosis ranged from 53% to 89% by state, showing that your options depend heavily on where you live7. Private insurance often includes similar categories, but may offer broader provider networks or cover different medications, sometimes with higher out-of-pocket costs. Consider Medicaid if you want lower cost-sharing and eligibility for state-run programs, but check your specific plan and state guidelines to clarify what’s included. Private insurance may suit those seeking more flexibility, but always confirm details about covered services and network restrictions before choosing a plan.

Can my employer find out if I use my health insurance for rehab?

No, your employer cannot access details about how you use your health insurance for rehab or wellness services. Privacy laws like HIPAA strictly protect your health information, which means your insurer can’t share specifics about your treatment with your workplace. While employers may see general data about plan usage—such as how many people use certain types of benefits—they do not receive any personal health details or information about individual claims1. This protection applies whether you use employer-sponsored insurance, Medicaid, or Marketplace plans. If you use paid leave or request workplace accommodations, you may need to provide basic documentation to HR, but the nature of your treatment remains confidential unless you choose to disclose it. This approach helps people feel safe using their insurance benefits for recovery and wellness support without fear of job-related consequences.

What’s the difference between in-network and out-of-network rehab coverage?

The main difference between in-network and out-of-network rehab coverage is how much your health insurance will pay and what you owe out-of-pocket. In-network providers have agreements with your insurer to accept set rates, which usually means lower costs and fewer billing surprises for you. Out-of-network rehab centers don’t have these agreements, so your plan may cover less—or sometimes nothing at all—and you could face much higher bills6. Studies reveal that claims for out-of-network services are far more likely to be denied, with in-network denial rates already ranging widely from 2% to 49% depending on the insurer6. This structure fits those who want predictable coverage and to avoid unexpected expenses: always confirm a provider’s network status before starting treatment to maximize your wellness benefits.

Will insurance cover virtual or telehealth treatment programs?

Yes, most health insurance plans do cover virtual or telehealth treatment programs for rehab and wellness support. Since 2023, telehealth has become a standard offering, with at least 38% of all behavioral health visits now taking place remotely—and insurers have responded by including coverage for online therapy, counseling, and outpatient rehab in both private and Medicaid plans2. This approach works best for individuals who need flexible scheduling, live in rural areas, or prefer the privacy of at-home care. Coverage details can still differ by insurer or state, so it’s wise to ask your health plan about approved telehealth providers, any session limits, and whether prior authorization is needed. Virtual support is now widely recognized as a cost-effective and accessible service, making it a practical option for anyone seeking recovery or overall wellness through their insurance benefits.

How long does the prior authorization process typically take?

The time it takes for prior authorization decisions with health insurance can vary, but most standard requests are processed within 5 to 14 business days after all paperwork is submitted. If your provider marks the request as urgent, some insurers will review it in as little as 24 to 72 hours9. Industry reports show that delays often come from missing information or follow-up questions, rather than active denials. This process fits situations where you need to plan your treatment start date, so it’s a good idea to check with both your insurer and provider for specific timelines. Always ask for confirmation when your request is received and follow up regularly to help avoid unnecessary waiting.

What happens if my insurance only covers part of my recommended treatment plan?

If your health insurance only pays for part of your recommended treatment plan, you’ll likely need to cover the remaining costs out-of-pocket or adjust your services to fit your benefits. Studies reveal that increased cost-sharing—like higher copays, deductibles, or session limits—is now the most common insurance barrier, with 40% of adults with chronic conditions reporting this issue in 20255. Some plans may only cover specific levels of rehab, a set number of sessions, or certain types of wellness support, while leaving others excluded. This situation fits people who want to maximize their coverage by prioritizing in-network providers and asking about sliding-scale fees or payment plans for anything not covered. You can also appeal for additional coverage if your provider believes more care is medically necessary. Always request a written explanation from your insurer about what’s included, and talk with your provider about ways to adjust your plan while still supporting your wellness goals.

Partner with Proven, Accessible Care

Understanding insurance coverage for addiction treatment represents just the first step—applying that knowledge to find accessible, quality care completes the journey. Throughout this article, we’ve explored how different insurance plans approach substance use treatment, what coverage typically includes, and how to assess whether a program aligns with your benefits. Now comes the practical application: partnering with a treatment provider who combines clinical excellence with insurance expertise.

Choosing the right treatment partner represents one of the most important decisions in the recovery journey. Quality care should combine evidence-based practices with compassionate support, delivered by professionals who understand both the complexities of addiction and the insurance landscape. Effective treatment programs offer comprehensive assessments that identify individual needs, followed by personalized care plans that address the physical, emotional, and behavioral aspects of substance use disorders. Medical supervision ensures safety during detoxification, while therapeutic interventions provide the tools necessary for long-term success.

The coverage assessment framework discussed earlier—evaluating deductibles, copayments, network status, and medical necessity requirements—becomes most valuable when paired with a treatment center that handles insurance verification proactively. Look for providers who offer dedicated insurance specialists to confirm your benefits before admission, explain your financial responsibility clearly, and work directly with your insurance company throughout treatment. This support transforms abstract policy language into concrete answers about what you’ll actually pay and what services your plan will cover.

Accessibility matters just as much as expertise. Treatment should fit into real life, not require putting everything on hold indefinitely. Flexible scheduling options, including outpatient programs that allow individuals to maintain work and family commitments, make recovery achievable for those who cannot step away from their responsibilities. Multiple levels of care—from medically supervised detox through outpatient counseling—ensure that as your needs change, your coverage can adapt accordingly within the same trusted treatment system.

If questions remain about your specific coverage, treatment duration, or out-of-pocket costs, don’t navigate those uncertainties alone. Contact treatment providers directly for a confidential insurance verification that clarifies exactly what your plan covers and identifies any potential gaps before you begin. Recovery becomes possible when individuals connect with the right resources at the right time—resources that combine accessible, professional care with the insurance knowledge that makes treatment financially feasible. Taking the first step toward verifying your coverage opens the door to a healthier, more fulfilling future free from the constraints of addiction.

References

- Mental health & substance abuse coverage – HealthCare.gov. https://www.healthcare.gov/coverage/mental-health-substance-abuse-coverage/

- Insurance Reimbursement Rates for Addiction Treatment. https://behavehealth.com/blog/insurance-reimbursement-rates-addiction-treatment

- The Mental Health Parity and Addiction Equity Act (MHPAEA) – CMS. https://www.cms.gov/marketplace/private-health-insurance/mental-health-parity-addiction-equity

- Gaps and barriers in drug and alcohol treatment following Affordable Care Act – NIH. https://pmc.ncbi.nlm.nih.gov/articles/PMC9835109/

- Patients report more health insurance barriers to care than last year – PAN Foundation. https://www.panfoundation.org/patients-facing-more-health-insurance-barriers-to-accessing-medications-and-treatment/

- Claims Denials and Appeals in ACA Marketplace Plans in 2021 – KFF. https://www.kff.org/private-insurance/claims-denials-and-appeals-in-aca-marketplace-plans/

- SUD Treatment in Medicaid: Variation by Service Type, Demographics, States, and Spending – KFF. https://www.kff.org/mental-health/sud-treatment-in-medicaid-variation-by-service-type-demographics-states-and-spending/

- Insurance barriers to substance use disorder treatment after Affordable Care Act implementation – NIH. https://pmc.ncbi.nlm.nih.gov/articles/PMC9948907/

- I Just Got Denied Coverage: How to File an Insurance Appeal for Substance Use Disorder – Partnership to End Addiction. https://drugfree.org/article/i-just-got-denied-coverage-now-what-how-to-file-an-insurance-appeal-for-substance-use-disorder/”

- The cost of addiction: Opioid use disorder in the United States – Avalere Health. https://advisory.avalerehealth.com/wp-content/uploads/2025/05/Avalere-Health-White-Paper_The-cost-of-opioid-addiction_OUD-in-the-United-States.pdf